U.S.-Asia Business

Leading the Charge: China’s Electric Vehicle Market

By Daniel Allen

China's burgeoning electric vehicle market offers risks and rewards.

After years of double-digit growth, China's auto market is widely expected to cool over the next few years, yet one segment is now bucking the trend. Electric Vehicles (EVs) and New Energy Vehicles (NEVs) have caught on in a big way in China, and have already made China the largest EV market in the world.

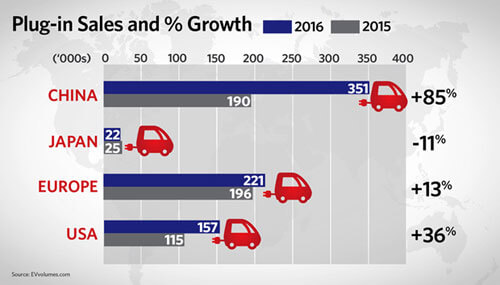

Chinese EV sales for 2016 were up 85 percent year-on-year to just over 350,000 cars, or 46 percent of the global total. This scale of growth is significantly higher than in any other large economy. Eager to drive further growth, the Chinese government has set a goal of 3 million domestic EV sales by 2025.

Many Chinese automotive companies are pumping huge sums into the NEV sector, which includes vehicles that are partially or fully powered by electricity, such as battery electric vehicles (BEVs) and plug-in hybrids (PHEVs). SAIC Motor, China's largest automaker, plans to invest $3 billion in new-energy cars in the period until 2020, and is targeting an annual sales volume of 600,000 cars.

Many well-known, foreign automakers have already entered the Chinese NEV market, including Tesla, General Motors, Nissan and BMW. While they remain slightly behind the curve, many are planning to launch China-focused, more competitively priced hybrid and fully-electric models over the next years.

"By 2020, we believe the government's current EV market push will no longer be needed," says Bill Russo, managing director and automotive practice leader at Shanghai-based Gao Feng Advisory Company. "Investment in core component technology, especially in battery production, along with the mass adoption of EVs, will force a 'tipping point,' when electrification is solely driven by market forces."

Push and pull

The reasons for Chinese EV market growth are numerous. Beijing wants to establish global leadership in NEV development and manufacturing, and has placed electric vehicle product and component development and production at the center of industrial policy.

"With China suffering from severe environmental pressures, air quality is clearly a major driver," says Jean-François Bélorgey, head of the automotive industry for EY France and part of EY's Global Automotive & Transportation Center. "Another critical issue is energy security. The increasing adoption of EVs will help China to reduce its huge dependence on imported oil."

"The increasing adoption of EVs will help China to reduce its huge dependence on imported oil."

On the demand side, the whirlwind rise of China's on-demand mobility sector is driving a higher mix of EVs in service fleets due to lower maintenance and fuel costs. In addition, easier access to license plates has also acted as an incentive for both individual and fleet purchases of electric cars.

On the supply side, the early adoption of EVs has been driven by government subsidies. This has been complemented by the ongoing development of supply-chain capabilities in areas such as batteries, battery management systems and electric motors.

"The capacity for Chinese companies to serve the domestic EV market, especially in terms of batteries and battery technology, is now scaling up very rapidly," says Russo.

A carrot-to-stick approach

Following the discovery of large-scale fraud within the Chinese system of NEV subsidies, Beijing has come up with a new, two-fold approach for the stimulation of EV manufacturing and sales.

The first proposal features a carbon credit scheme, which looks likely to be enforced from 2018. According to the scheme, NEV "credits" must account for 8 percent of an automaker's total car production by 2018, 10 percent by 2019, and 12 percent by 2020. The credit value of different NEVs will vary according to their mileage on one charge—this is designed to encourage NEV manufacturers to extend the range of their electric cars.

A second proposal would put a cap on average fleet fuel consumption, with extra credits for NEVs. This scheme would oblige all automakers selling conventional fuel vehicles to also sell NEVs, and means that those foreign car manufacturers yet to launch a NEV in China would be forced to do so.

Beijing has also taken steps to limit the licenses available to Chinese EV manufacturers. In an effort to consolidate and weed out the weakest players, the Ministry of Industry and Information Technology (MIIT) recently announced a restriction on the granting of licenses to new EV startups, limiting the number to just 10 per year. Established automakers such as SAIC Motor and BYD are exempted.

"All of these changes show that Beijing isn't just looking to meet its EV targets on paper," says Julia Coym, a senior China analyst at global consulting firm Control Risks and Chinese auto sector expert. "Rather than another uncompetitive, overcapacity-plagued sector, it wants to grow a successful and Chinese-led domestic EV industry."

Challenges and opportunities

Uncertainty around technology transfer and overall market access is a big concern for foreign players in China's EV industry. A raft of EV battery standards released late in 2016 is symptomatic of a wider campaign to support the competitiveness of domestic firms in the EV space.

Chinese automakers have largely struggled to compete with their foreign peers in conventional fuel vehicles, both in China and abroad. Going forward, it is more than likely that Beijing will continue in its attempts to boost competitiveness in the domestic EV manufacturing sector. This will involve the introduction of other technical specifications that reflect technological solutions being pursued by Chinese companies, rather than approaches favored by their foreign competitors.

"China still wants foreign investment in the EV space, but revisions to EV-related regulations favoring local companies, either real or perceived, will increasingly prompt vocal opposition from foreign manufacturers and their governments," says Coym. "The term 'reciprocity' is likely to be thrown around more frequently, even by countries like Germany."

Despite these barriers, there are still opportunities for Western firms in China's EV industry, with the market evolving rapidly and the competitive landscape still in its early stages of development. Falling government subsidies are now seeing the price of domestic EV brands increase, raising the competitiveness of their foreign counterparts.

Early movers are already taking steps to leverage Chinese demand. Volkswagen has recently announced a joint venture with Chinese automaker JAC, which will see the launch and mass production of a new, small NEV in 2018.

"The main opportunity for all companies involved in the EV sector is clearly the size of the Chinese market," says Bélorgey. "It's really all about scale. China will help Western OEMs [original equipment manufacturers] develop their own capabilities and products by allowing them to better recover the large investments that they have to make on the technology."

The key challenge for foreign players is understanding China's unique EV market in terms of its mobility users, their pain points and changing habits, Beijing's influence and enforced collaboration with local players, and the proliferation of disruptive players.

"With Tencent and JD.com both investing in Chinese electric car startup NextEV, even non-traditional players from the digital space are getting involved," says Russo.

Each value chain in China's EV market presents it own challenges and opportunities, but the boundaries between sectors are blurring, and creating a winning solution cannot be done single-handedly.

"'Co-opetition' is the norm in China, and players must embrace this," adds Russo. "It's about embracing the ecosystem concept and embracing your partners, even competitors, in the ecosystem."

Battery blitz

Auto manufacturers are not the only companies poised to benefit from China's burgeoning NEV sector. Despite market restrictions, opportunities also exist in battery manufacturing. Last year, changes to Chinese legislation allowed foreign firms to set up wholly-owned electric vehicle battery manufacturing plants in free-trade zones in Shanghai, Guangdong, Tianjin and Fujian.

North American companies are already looking to leverage opportunities presented by China's EV battery market. New York-headquartered Plug Power recently announced the signing of a memorandum of understanding with two Chinese companies to pursue the development of hydrogen fuel cell solutions for electric vehicles. In 2017, the three companies expect to deliver two industrial delivery truck prototypes, featuring Plug Power's fuel cell engines. Last September, Canadian hydrogen fuel cell designer and manufacturer Ballard Power Systems announced the commissioning and deployment of 12 fuel cell-powered buses in the Chinese city of Foshan. According to Ballard, this is the initial deployment of a planned 300 fuel cell-powered buses.

While China is gradually opening up its EV battery market, conditions still greatly favor domestic suppliers. With government support, Chinese battery suppliers are increasingly building a strong business case to compete with foreign players and become the primary global suppliers for OEMs.

"Chinese companies are collaborating at a level we have never seen before in developing innovative, battery-related solutions," says Russo. "We expect by 2020 that China will account for over half of the global battery production capacity."

Infrastructure investment

The development of China's EV infrastructure should also see burgeoning opportunities for Western companies.

With the ideal ratio of charging interfaces to new energy vehicles seen as around 1:1, the roll-out of charging pillars in China needs to rapidly accelerate. While government targets and financial incentives to reach them have so far underpinned EV sales growth, consumer demand has lagged behind, partly as a result of issues such as the fear of being stranded by a flat battery.

Addressing this issue, Beijing recently announced a plan to build 10,000 public fast-charging stations and 120,000 charging pillars along the country's expressways. These installations will service over 200 cities and 22,000 miles of road. According to Hong Kong-based HKTDC Research, the mainland charging facilities market was worth RMB40 billion ($5.7 billion) by the end of last year, and is projected to exceed RMB100 billion ($14.4 billion) by 2020.

"So far, China's charging pillar ecosystem has lagged far behind demand," says Marco Hecker, Deloitte China's auto sector consulting leader. "The margins here are undoubtedly low. But in terms of companies going in there and developing it, it's still largely up for grabs."