U.S.-Asia Business

How Hollywood Can Still Capitalize on the Chinese Market

East West Bank CEO Dominic Ng pinpoints future opportunities for Hollywood-China cooperation.

Chinese direct investment in the U.S. entertainment industry has gone from boom to bust in the past year, and many are wondering about the future. Some think this drop is a death knell for China-U.S. entertainment collaboration, but I think that ignores the bigger picture. The fundamentals continue to support greater cooperation between Chinese and U.S. entertainment companies, and U.S. businesses can still benefit from collaboration with Chinese investors in the current environment, if they know the right approach.

From boom to bust

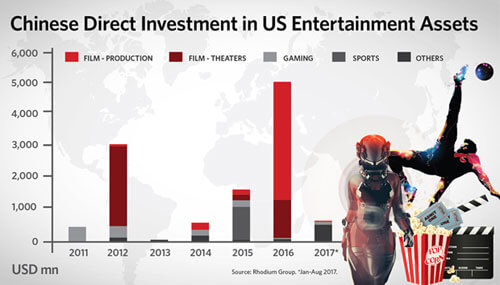

In past years, entertainment had become one of the hottest areas for Chinese direct investment in the U.S., particularly through acquisitions. Annual flows reached a staggering $5 billion in 2016, or more than 10 percent of all Chinese direct investment in the United States. However, 2017 has seen a dramatic reversal of this trend, with year-to-date entertainment investment falling to less than $500 million.

Chinese direct investment in US entertainment assets

Film-related direct investment has been particularly impacted, dropping by $4.6 billion from 2016 so far in 2017. Several high profile deals have collapsed in the last year, including Anhui Xinke’s $345 million purchase of Voltage Pictures, Wanda’s $1 billion purchase of Dick Clark Productions, and Recon Holdings’ $100 million deal for Millennium Films. No major new acquisitions have been announced since February 2017.

Short-term policy headwinds

What is responsible for this drop in Chinese entertainment investment? In short, it has become very difficult for buyers to obtain Chinese authorities’ approval for overseas entertainment purchases. After watching Chinese foreign exchange reserves fall by hundreds of billions of dollars, Chinese regulators became convinced in late 2016 that too much capital was leaving the country. To stem these outflows, Beijing introduced capital controls, including on foreign direct investment. As a result, Chinese overseas mergers and acquisitions took a hit across the board in early 2017, as it became increasingly difficult to get money out of China.

"U.S. businesses can still benefit from collaboration with Chinese investors in the current environment, if they know the right approach."

Beijing became particularly concerned about overseas investments with questionable commercial viability, which applies to many attempted acquisitions in the U.S. entertainment sector. Many deals were driven by financial arbitrage and speculation. For example, Wanda agreed to pay $3.5 billion for Legendary Entertainment in 2016 because it wanted to re-list Legendary in China at a higher valuation (while the average PE ratio of US-listed film studios is around 20, film studios listed in China typically trade with a PE ratio north of 30). Other companies with no experience in the entertainment industry jumped on the bandwagon under the auspice of diversification—for example, the acquisition of Voltage Pictures by Anhui Xinke, a copper materials company with no film industry experience.

These concerns led Chinese authorities to place deals in real estate, hotels, cinemas, entertainment and related areas on a “Restricted List.” As a result, overseas entertainment purchases now face a much higher level of scrutiny. Chinese buyers must convince regulators that investments are aligned with buyers’ core areas of business, reasonably priced and ultimately likely to be profitable. Vanity deals, acquisitions with inflated valuations, and investments motivated by short-term financial considerations can no longer be expected to pass muster with Chinese authorities.

Economic fundamentals

Despite these short-term problems, I remain optimistic about U.S.-China cooperation in film and other entertainment sectors. For one, macroeconomic headwinds have already calmed and will eventually abate. China’s external macroeconomic environment has improved in the first half of 2017. Capital outflows have stabilized, and Beijing is no longer seeing tens of billions of dollars leave its shores each month.

Two, the Chinese government has clarified that it will continue to support overseas direct investments that strengthen investors’ core capabilities. Beijing is aware that overseas presences are critical for Chinese companies to compete globally, and current regulations are mostly geared toward suppressing speculative and irrational deals. This “correction” could ultimately benefit Chinese investors with professional deal teams and a long-term perspective on synergies.

Three, and most importantly, the commercial rationale for Chinese engagement in the American entertainment industry remains as strong as ever. PwC projects that China’s Entertainment and Media sector will grow from $186 billion in 2016 to $258 billion by 2020, with cinema being the fastest-growing segment. Looking at the supply side, the United States remains the unrivaled global champion in producing high-quality entertainment content. Ninety-nine of the top 100 worldwide grossing films of all time are American. The world’s 12 most-visited theme parks are all owned by American companies. Serving the growth in Chinese entertainment demand with a supply of high-quality U.S. content and experience is a no-brainer for any Chinese investor.

How the U.S. entertainment industry can still capitalize on the Chinese market

The days of high-flying Chinese buyers paying huge premiums for U.S. entertainment firms are clearly over. How can U.S. investors and companies seeking Chinese partners position themselves to navigate the current environment? In my view, the following strategies make sense:

First, if you seek Chinese equity investors, smaller strategic deals are better. Many entertainment investments in the last few years have been driven by herd movement and the search for short-term financial returns. With Beijing taking a harder stance against these bets, investors need to focus on strategic investments with sound commercial logic instead of valuation differentials. Beijing will also continue frowning on “trophy hunting,” or Chinese firms purchasing foreign assets for prestige regardless of price. In the current environment, Chinese firms will find it easier to pursue smaller strategic deals. While larger acquisitions floundered, smaller deals—Puji Capital’s Mandalay Endurance Media joint venture and Fosun’s purchase of Blue Man Group—have successfully closed this year.

"Streaming will only increase in importance, and since Wi-Fi is widely available in Chinese cities, the possibilities for viewing short content are endless."

Second, licensing, slate financing and other channels are good alternatives to equity investments. While acquisition activity has dropped sharply, Chinese capital continues to flow to the U.S. through other channels. Despite occasional hiccups (for example, Paramount’s partnership with Huahua and Shanghai Film), passive slate financing deals continue to produce American films with economic upside for Chinese studios, like Bona’s investment in Fox’s live-action movie slate, which resulted in the international hit “The Martian,” and Huayi Bros.’ deal with STX entertainment.

Another option is the co-production model, which offers Chinese and American parties an opportunity to collaborate without a prolonged commitment. When it comes to co-productions, some say it is impossible to make a film that appeals to both U.S. and Chinese audiences, pointing to the disappointing performance of “The Great Wall.” However, many are now watching the much lower budget action drama “The Foreigner” starring Jackie Chan and Pierce Brosnan. The STX Entertainment release cost only $35 million to make, and so far has grossed more than $117 million in ticket sales worldwide; evidence that, with the right budget and the right talent with worldwide appeal, a profitable co-production is possible. The opportunity for further improvements upon this model is worth exploring.

Licensing content is another avenue. This method allows Chinese investors to make informed decisions on targeted brands and content based on actual Chinese demand, and the sheer size of China’s domestic market gives Chinese firms a lot of power to compete in bidding. Alibaba’s recent deal with the Pac-12 Conference to stream college sports in China is an example of this approach.

Third, U.S. entertainment firms should reevaluate opportunities for expanding their Chinese footprints. While China has become more careful about capital outflows, it is more eager than ever to attract foreign investment. Several U.S. entertainment companies have shown that local operations in China can pay off if done smartly. One example is Disney, which drew more than 11 million visitors to its new Shanghai Disneyland joint venture in 2016, exceeding the company's most optimistic expectations. Warner Bros.’ Chinese joint venture with China Media Capital—Flagship Entertainment Group Limited—is a pioneer trying to build this success in film. The company is working on a slate of 12 movies for the Chinese market. Some restrictions on foreign ownership in media and entertainment will likely remain, but I expect to see greater leeway for U.S. investors to acquire Chinese assets or engage in joint ventures in coming years. There’s also a good chance for China to increase its annual foreign film quota and give foreign movies more favorable release dates.

Fourth, U.S. studios need to develop an understanding and long-term vision of Chinese demand. The best way to capitalize on Chinese consumers is to understand what Chinese consumers want, and create capabilities to serve that demand. The money will follow. U.S. executives also need to be up to speed with Chinese distribution platforms, particularly mobile. There are hundreds of millions of smartphone-connected eyes in China hungry for U.S. content, and firms with the right Chinese technology partnerships could better serve them. Focusing solely on the silver screen ignores a huge portion of the available Chinese market. Streaming will only increase in importance, and, since Wi-Fi is widely available in Chinese cities, the opportunities for viewing short content are endless, from the subways to driverless cars. Forming partnerships with Chinese tech companies such as Baidu, Alibaba, and Tencent would be crucial to reaching that mobile audience. Reality shows are also an area of growth and highly popular in China, with more than 100 reality programs currently available on Mainland satellite channels.

Conclusions

There are ample opportunities for continued U.S.-China entertainment collaboration, through both direct investment and other models. To take advantage of these opportunities, American executives need to better understand the Chinese market, consumption preferences and regulatory direction, including through more intentional engagement with Chinese firms and ventures. The greatest future opportunities for American firms involve reaching more Chinese consumers in the ways they want to consume content.